Exploding debt threatens America. By John Taylor

FT, May 26 2009 20:48

Standard and Poor’s decision to downgrade its outlook for British sovereign debt from “stable” to “negative” should be a wake-up call for the US Congress and administration. Let us hope they wake up.

Under President Barack Obama’s budget plan, the federal debt is exploding. To be precise, it is rising – and will continue to rise – much faster than gross domestic product, a measure of America’s ability to service it. The federal debt was equivalent to 41 per cent of GDP at the end of 2008; the Congressional Budget Office projects it will increase to 82 per cent of GDP in 10 years. With no change in policy, it could hit 100 per cent of GDP in just another five years.

“A government debt burden of that [100 per cent] level, if sustained, would in Standard & Poor’s view be incompatible with a triple A rating,” as the risk rating agency stated last week.

I believe the risk posed by this debt is systemic and could do more damage to the economy than the recent financial crisis. To understand the size of the risk, take a look at the numbers that Standard and Poor’s considers. The deficit in 2019 is expected by the CBO to be $1,200bn (€859bn, £754bn). Income tax revenues are expected to be about $2,000bn that year, so a permanent 60 per cent across-the-board tax increase would be required to balance the budget. Clearly this will not and should not happen. So how else can debt service payments be brought down as a share of GDP?

Inflation will do it. But how much? To bring the debt-to-GDP ratio down to the same level as at the end of 2008 would take a doubling of prices. That 100 per cent increase would make nominal GDP twice as high and thus cut the debt-to-GDP ratio in half, back to 41 from 82 per cent. A 100 per cent increase in the price level means about 10 per cent inflation for 10 years. But it would not be that smooth – probably more like the great inflation of the late 1960s and 1970s with boom followed by bust and recession every three or four years, and a successively higher inflation rate after each recession.

The fact that the Federal Reserve is now buying longer-term Treasuries in an effort to keep Treasury yields low adds credibility to this scary story, because it suggests that the debt will be monetised. That the Fed may have a difficult task reducing its own ballooning balance sheet to prevent inflation increases the risks considerably. And 100 per cent inflation would, of course, mean a 100 per cent depreciation of the dollar. Americans would have to pay $2.80 for a euro; the Japanese could buy a dollar for Y50; and gold would be $2,000 per ounce. This is not a forecast, because policy can change; rather it is an indication of how much systemic risk the government is now creating.

Why might Washington sleep through this wake-up call? You can already hear the excuses.

“We have an unprecedented financial crisis and we must run unprecedented deficits.” While there is debate about whether a large deficit today provides economic stimulus, there is no economic theory or evidence that shows that deficits in five or 10 years will help to get us out of this recession. Such thinking is irresponsible. If you believe deficits are good in bad times, then the responsible policy is to try to balance the budget in good times. The CBO projects that the economy will be back to delivering on its potential growth by 2014. A responsible budget would lay out proposals for balancing the budget by then rather than aim for trillion-dollar deficits.

“But we will cut the deficit in half.” CBO analysts project that the deficit will be the same in 2019 as the administration estimates for 2010, a zero per cent cut.

“We inherited this mess.” The debt was 41 per cent of GDP at the end of 1988, President Ronald Reagan’s last year in office, the same as at the end of 2008, President George W. Bush’s last year in office. If one thinks policies from Reagan to Bush were mistakes does it make any sense to double down on those mistakes, as with the 80 per cent debt-to-GDP level projected when Mr Obama leaves office?

The time for such excuses is over. They paint a picture of a government that is not working, one that creates risks rather than reduces them. Good government should be a nonpartisan issue. I have written that government actions and interventions in the past several years caused, prolonged and worsened the financial crisis. The problem is that policy is getting worse not better. Top government officials, including the heads of the US Treasury, the Fed, the Federal Deposit Insurance Corporation and the Securities and Exchange Commission are calling for the creation of a powerful systemic risk regulator to reign in systemic risk in the private sector. But their government is now the most serious source of systemic risk.

The good news is that it is not too late. There is time to wake up, to make a mid-course correction, to get back on track. Many blame the rating agencies for not telling us about systemic risks in the private sector that lead to this crisis. Let us not ignore them when they try to tell us about the risks in the government sector that will lead to the next one.

The writer, a professor of economics at Stanford and a senior fellow at the Hoover Institution, is the author of ‘Getting Off Track: How Government Actions and Interventions Caused, Prolonged, and Worsened the Financial Crisis’

Tuesday, May 26, 2009

GM's new owner (the Obama administration) should stop bullying the company's bondholders

Government Motors. WaPo Editorial

GM's new owner (the Obama administration) should stop bullying the company's bondholders.

WaPo, Tuesday, May 26, 2009

IN THEORY, a government bailout should provide a short-term infusion of cash to give a struggling company the chance to right itself. But in its aggressive dealings with U.S. automakers, most recently General Motors, the Obama administration is coming dangerously close to engaging in financial engineering that ignores basic principles of fairness and economic realities to further political goals.

It is now clear that there is no real difference between the government and the entity that identifies itself as GM. For all intents and purposes, the government, which is set to assume a 50 percent equity stake in the company, is GM, and it has been calling the shots in negotiations with creditors. While the Obama administration has been playing hardball with bondholders, it has been more than happy to play nice with the United Auto Workers. How else to explain why a retiree health-care fund controlled by the UAW is slated to get a 39 percent equity stake in GM for its remaining $10 billion in claims while bondholders are being pressured to take a 10 percent stake for their $27 billion? It's highly unlikely that the auto industry professionals at GM would have cut such a deal had the government not been standing over them -- or providing the steady stream of taxpayer dollars needed to keep the factory doors open.

GM is widely expected to file for bankruptcy before the end of this month. If this were a typical bankruptcy, the company would be allowed by law to tear up its UAW collective bargaining agreement and negotiate for drastically reduced wages and benefits. That's not going happen. Phrased another way: The government won't let that happen. Still, the threat of a contract abrogation probably played a role in the union's agreement to cost-cutting measures last week. (The details of the deal have not been made public; union members are scheduled to vote on the proposal early this week.) It's never easy for unions to make concessions, but the sting of handing back money is being softened by the government's desire to give the union a huge ownership stake in GM. Might bondholders be more willing to agree to the kind of quick restructuring the government hopes for if they had been treated more fairly from the outset?

The administration argues that it could not risk alienating the union for fear of triggering a walkout that could permanently cripple GM. It also posits that it had to agree to protect suppliers and fund warranties in order to preserve jobs and reassure prospective buyers that their cars would be serviced. These are legitimate concerns. But it's too bad that the Obama administration has not thought more deeply about how its bullying of bondholders could convince future investors that the last thing they want to do is put money into any company that the government has -- or could -- become involved in.

GM's new owner (the Obama administration) should stop bullying the company's bondholders.

WaPo, Tuesday, May 26, 2009

IN THEORY, a government bailout should provide a short-term infusion of cash to give a struggling company the chance to right itself. But in its aggressive dealings with U.S. automakers, most recently General Motors, the Obama administration is coming dangerously close to engaging in financial engineering that ignores basic principles of fairness and economic realities to further political goals.

It is now clear that there is no real difference between the government and the entity that identifies itself as GM. For all intents and purposes, the government, which is set to assume a 50 percent equity stake in the company, is GM, and it has been calling the shots in negotiations with creditors. While the Obama administration has been playing hardball with bondholders, it has been more than happy to play nice with the United Auto Workers. How else to explain why a retiree health-care fund controlled by the UAW is slated to get a 39 percent equity stake in GM for its remaining $10 billion in claims while bondholders are being pressured to take a 10 percent stake for their $27 billion? It's highly unlikely that the auto industry professionals at GM would have cut such a deal had the government not been standing over them -- or providing the steady stream of taxpayer dollars needed to keep the factory doors open.

GM is widely expected to file for bankruptcy before the end of this month. If this were a typical bankruptcy, the company would be allowed by law to tear up its UAW collective bargaining agreement and negotiate for drastically reduced wages and benefits. That's not going happen. Phrased another way: The government won't let that happen. Still, the threat of a contract abrogation probably played a role in the union's agreement to cost-cutting measures last week. (The details of the deal have not been made public; union members are scheduled to vote on the proposal early this week.) It's never easy for unions to make concessions, but the sting of handing back money is being softened by the government's desire to give the union a huge ownership stake in GM. Might bondholders be more willing to agree to the kind of quick restructuring the government hopes for if they had been treated more fairly from the outset?

The administration argues that it could not risk alienating the union for fear of triggering a walkout that could permanently cripple GM. It also posits that it had to agree to protect suppliers and fund warranties in order to preserve jobs and reassure prospective buyers that their cars would be serviced. These are legitimate concerns. But it's too bad that the Obama administration has not thought more deeply about how its bullying of bondholders could convince future investors that the last thing they want to do is put money into any company that the government has -- or could -- become involved in.

Unilateral or Worldwide, Waxman-Markey Fails Standard Cost/Benefit Tests (CO2 “leakage” makes bad even worse)

Unilateral or Worldwide, Waxman-Markey Fails Standard Cost/Benefit Tests (CO2 “leakage” makes bad even worse). By Robert Murphy

Master Resource, May 26, 2009

Jim Manzi has a very good post introducing the analysis of costs and benefits of Waxman-Markey. Here I want to follow up on Manzi’s great start, by showing that Chip Knappenberger’s estimate of the climate benefits of Waxman-Markey (W-M) actually erred on the side of optimism in its assumptions.

Specifically, Knappenberger very conservatively ignored the problem of “leakage”–he didn’t model the fact that unilateral U.S. carbon caps would actually increase the rate at which other countries’ own emissions grow. What’s worse, even if the entire world signed on to the aggressive emission schedule in W-M, the resulting environmental benefits would be achieved at a staggering cost in terms of lost economic output.

No matter how you slice it–whether the U.S. goes it alone, or the rest of the world signs on too–the environmental benefits of W-M are swamped by its economic costs.

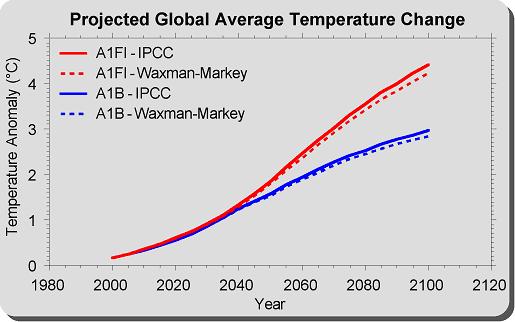

“Leakage”–An Important Variable. In a MasterResource post that has become a touchstone of the great climate debate, Chip Knappenberger used a standard model to assess the expected reductions in global mean temperatures if the U.S. faithfully adhered to the emission targets in W-M. Knappenberger found that by 2100, the projected global warming under two different “baseline” emission scenarios would be postponed by a handful of years.

The pro-interventionist scientists at RealClimate have conceded the basic validity of Chip’s analysis; they simply accuse him of rigging the game by considering unilateral U.S. action.

The pro-interventionist scientists at RealClimate have conceded the basic validity of Chip’s analysis; they simply accuse him of rigging the game by considering unilateral U.S. action.

What is interesting is that Chip did not assume that the emissions of the rest of the world would grow more quickly because of (the stipulated) unilateral U.S. committment to W-M. Yet this would surely happen, because of a phenomenon referred to in the climate economics literature as leakage. The intuition is quite simple: If the U.S. imposes a steep price on operations that emit carbon, then U.S. industries will produce fewer carbon-intensive goods and services. (That’s the whole point, after all.)

Yet because of the reduction in output of these sectors, the world price of these items will tend to rise, which in turn will call forth greater output from (carbon-intensive) sectors in the unregulated countries.

I caution readers that some cynics of government action to limit climate change draw an unwarranted conclusion from this type of analysis. I have heard such critics say things like, “This is ridiculous! If the U.S. goes it alone, all we’ll do is ship all of our jobs to China, and we won’t affect global emissions one iota.”

Strictly speaking, that is taking it too far. For various reasons, it is not true that every cutback in carbon-intensive production in the U.S. would be perfectly offset by expanded production in an unregulated jurisdiction. However, even though there won’t be a one-for-one offset in terms of final goods produced, the relative carbon emissions is a different matter. This is because Chinese manufacturing operations emit more tons of carbon than American factories do, in order to produce the same physical amount of goods.

Hence, the amount of “leakage” resulting from a unilateral U.S. emissions cap is ultimately an empirical matter, but it would probably be very significant. To repeat, Chip’s analysis (described above) did not take this effect into account. Chip merely took two standard IPCC baseline emission scenarios, and then altered them by reducing the baseline growth in U.S. emissions in order to comply with the targets in W-M. He is consequently overestimating the environmental benefits of unilateral American adherence to the emission targets in W-M. In other words, the dotted lines in the chart above would be even closer to the solid lines, once the model took into account the superior profitability of Chinese carbon-intensive operations after the U.S. government hobbled American operations.

Leakage in the Context of the “Social Cost of Carbon.” Some of the more sophisticated critics of Chip’s analysis asked a reasonable question: Since plenty of economic models show a “social cost of carbon” emissions, it doesn’t really matter what the rest of the world does, right? After all, if emitting an extra ton of carbon today, translates into a (present discounted value of) an expected increase in future climate change damages of (say) $35, then it surely moves us in the direction of efficiency if the U.S. government slaps a penalty on domestic emitters, right?

There are two problems here. First, nobody is defending Waxman-Markey on the basis of cost/benefit analysis, because it can’t be done. There is a bit of a problem in comparing apples with apples (since the integrated assessment models gauging the impact of mitigation policies all assume concerted worldwide action), but it is safe to say that the emissions targets in W-M are far too aggressive, if we are going to be guided by the “social cost of carbon.”

For example, Table 3.10 (page 229) of Working Group III’s contribution to the IPCC Fourth Assessment Report (.pdf) shows that of 177 scenarios surveyed from the peer-reviewed literature, only 6 scenarios assumed worldwide emissions reductions in the steepest category of 50% - 85% by the year 2050. (Recall that W-M imposes a reduction of 83% by 2050. But note that the IPCC reductions are relative to 2000 emissions, while W-M’s 83% target is relative to 2005 emissions.)

If we turn to the specific DICE model by William Nordhaus–who is a pioneer and leader in this field, and who is a definite proponent of a carbon tax–we see that the aggressive emission cutbacks in W-M fail his cost/benefit test by a wide mark. The IPCC’s Table 3.10 and Nordhaus’s own results agree that capping emissions in 2050 at 83% below current levels, would correspond to Nordhaus’s estimates of a policy of capping atmospheric concentrations at no more than 1.5x preindustrial levels. (See Nordhaus’s Table 5-5, p. 96 here [.pdf]. Note that we are being conservative with our choice, because the steep emission cuts in W-M are arguably closer to the “Gore proposal,” which the DICE model finds even more destructive than the policy that we have instead chosen as a surrogate for W-M.)

Yet according to Nordhaus’s DICE model, such an aggressive policy would do far more harm to the economy, than it would yield in benefits of averted climate damage. Specifically, Nordhaus estimates that the policy corresponding to W-M targets would make the world some $15 trillion poorer relative to the business-as-usual baseline of no controls (see Table 5-1, page 82, here [.pdf]). Yes, worldwide commitment to the aggressive emission schedule in W-M would avert climate damages that would otherwise occur, which DICE values as a benefit of $12.6 trillion. But the draconian emission caps would require $27.24 trillion in abatement (compliance) costs. Thus the environmental benefits are swamped by the economic costs.

So we see that using the standard “social costs of carbon” approach, reveals that W-M imposes far too high a price on carbon emissions than is warranted by this Pigovian framework. That is why proponents of steep emission cuts must abandon standard cost/benefit analysis, and instead recommend particular environmental targets (such as stabilizing atmospheric concentrations at a presumed “safe” level) and then try to find the least-cost method of attaining them.

As a final point, we should note how the problem of leakage also influences the “social cost of carbon” as computed in various models. When Nordhaus or other economists calculate the social cost of carbon (SCC), they are asking what happens to the present discounted value of future environmental damages, if someone emits an additional ton of carbon today, while holding the assumed trajectory of all future emissions constant.

Now we see the weakness in this metric, when trying to assess the net benefits of unilateral climate policy. Once we take leakage into account, we see that the standard measure of SCC overstates (possibly grossly so) the true costs to society from an additional unit of emissions. In reality, there are two things going on: When a U.S. manufacturer produces more units of a carbon-intensive good, it is true that he emits more carbon dioxide into the atmosphere. This is what the SCC looks at, and judges him accordingly.

However, the U.S. manufacturer also pushes down the world price of the good in question, and that tends to cause other producers to emit less CO2. Thus, there is a positive externality laid on top of the negative externality. The greater the scope for leakage, the greater the positive externality. In the extreme, where U.S. operations would be completely outsourced to China (in terms of carbon emissions, if not output of final goods), then the correctly measured “social cost of carbon” for U.S. operations would be zero, in the context of a unilateral U.S. cap.

Conclusion. Here are the takeaway messages:

Yet W-M proponents have done none of these things. Surely they could at least try–even in an informal blog post–to formalize their case, before expecting the American people to sign on to a plan that could cost trillions of dollars in forfeited economic growth, and which on its face will do very little to alter the course of global warming.

Master Resource, May 26, 2009

Jim Manzi has a very good post introducing the analysis of costs and benefits of Waxman-Markey. Here I want to follow up on Manzi’s great start, by showing that Chip Knappenberger’s estimate of the climate benefits of Waxman-Markey (W-M) actually erred on the side of optimism in its assumptions.

Specifically, Knappenberger very conservatively ignored the problem of “leakage”–he didn’t model the fact that unilateral U.S. carbon caps would actually increase the rate at which other countries’ own emissions grow. What’s worse, even if the entire world signed on to the aggressive emission schedule in W-M, the resulting environmental benefits would be achieved at a staggering cost in terms of lost economic output.

No matter how you slice it–whether the U.S. goes it alone, or the rest of the world signs on too–the environmental benefits of W-M are swamped by its economic costs.

“Leakage”–An Important Variable. In a MasterResource post that has become a touchstone of the great climate debate, Chip Knappenberger used a standard model to assess the expected reductions in global mean temperatures if the U.S. faithfully adhered to the emission targets in W-M. Knappenberger found that by 2100, the projected global warming under two different “baseline” emission scenarios would be postponed by a handful of years.

The pro-interventionist scientists at RealClimate have conceded the basic validity of Chip’s analysis; they simply accuse him of rigging the game by considering unilateral U.S. action.

The pro-interventionist scientists at RealClimate have conceded the basic validity of Chip’s analysis; they simply accuse him of rigging the game by considering unilateral U.S. action.What is interesting is that Chip did not assume that the emissions of the rest of the world would grow more quickly because of (the stipulated) unilateral U.S. committment to W-M. Yet this would surely happen, because of a phenomenon referred to in the climate economics literature as leakage. The intuition is quite simple: If the U.S. imposes a steep price on operations that emit carbon, then U.S. industries will produce fewer carbon-intensive goods and services. (That’s the whole point, after all.)

Yet because of the reduction in output of these sectors, the world price of these items will tend to rise, which in turn will call forth greater output from (carbon-intensive) sectors in the unregulated countries.

I caution readers that some cynics of government action to limit climate change draw an unwarranted conclusion from this type of analysis. I have heard such critics say things like, “This is ridiculous! If the U.S. goes it alone, all we’ll do is ship all of our jobs to China, and we won’t affect global emissions one iota.”

Strictly speaking, that is taking it too far. For various reasons, it is not true that every cutback in carbon-intensive production in the U.S. would be perfectly offset by expanded production in an unregulated jurisdiction. However, even though there won’t be a one-for-one offset in terms of final goods produced, the relative carbon emissions is a different matter. This is because Chinese manufacturing operations emit more tons of carbon than American factories do, in order to produce the same physical amount of goods.

Hence, the amount of “leakage” resulting from a unilateral U.S. emissions cap is ultimately an empirical matter, but it would probably be very significant. To repeat, Chip’s analysis (described above) did not take this effect into account. Chip merely took two standard IPCC baseline emission scenarios, and then altered them by reducing the baseline growth in U.S. emissions in order to comply with the targets in W-M. He is consequently overestimating the environmental benefits of unilateral American adherence to the emission targets in W-M. In other words, the dotted lines in the chart above would be even closer to the solid lines, once the model took into account the superior profitability of Chinese carbon-intensive operations after the U.S. government hobbled American operations.

Leakage in the Context of the “Social Cost of Carbon.” Some of the more sophisticated critics of Chip’s analysis asked a reasonable question: Since plenty of economic models show a “social cost of carbon” emissions, it doesn’t really matter what the rest of the world does, right? After all, if emitting an extra ton of carbon today, translates into a (present discounted value of) an expected increase in future climate change damages of (say) $35, then it surely moves us in the direction of efficiency if the U.S. government slaps a penalty on domestic emitters, right?

There are two problems here. First, nobody is defending Waxman-Markey on the basis of cost/benefit analysis, because it can’t be done. There is a bit of a problem in comparing apples with apples (since the integrated assessment models gauging the impact of mitigation policies all assume concerted worldwide action), but it is safe to say that the emissions targets in W-M are far too aggressive, if we are going to be guided by the “social cost of carbon.”

For example, Table 3.10 (page 229) of Working Group III’s contribution to the IPCC Fourth Assessment Report (.pdf) shows that of 177 scenarios surveyed from the peer-reviewed literature, only 6 scenarios assumed worldwide emissions reductions in the steepest category of 50% - 85% by the year 2050. (Recall that W-M imposes a reduction of 83% by 2050. But note that the IPCC reductions are relative to 2000 emissions, while W-M’s 83% target is relative to 2005 emissions.)

If we turn to the specific DICE model by William Nordhaus–who is a pioneer and leader in this field, and who is a definite proponent of a carbon tax–we see that the aggressive emission cutbacks in W-M fail his cost/benefit test by a wide mark. The IPCC’s Table 3.10 and Nordhaus’s own results agree that capping emissions in 2050 at 83% below current levels, would correspond to Nordhaus’s estimates of a policy of capping atmospheric concentrations at no more than 1.5x preindustrial levels. (See Nordhaus’s Table 5-5, p. 96 here [.pdf]. Note that we are being conservative with our choice, because the steep emission cuts in W-M are arguably closer to the “Gore proposal,” which the DICE model finds even more destructive than the policy that we have instead chosen as a surrogate for W-M.)

Yet according to Nordhaus’s DICE model, such an aggressive policy would do far more harm to the economy, than it would yield in benefits of averted climate damage. Specifically, Nordhaus estimates that the policy corresponding to W-M targets would make the world some $15 trillion poorer relative to the business-as-usual baseline of no controls (see Table 5-1, page 82, here [.pdf]). Yes, worldwide commitment to the aggressive emission schedule in W-M would avert climate damages that would otherwise occur, which DICE values as a benefit of $12.6 trillion. But the draconian emission caps would require $27.24 trillion in abatement (compliance) costs. Thus the environmental benefits are swamped by the economic costs.

So we see that using the standard “social costs of carbon” approach, reveals that W-M imposes far too high a price on carbon emissions than is warranted by this Pigovian framework. That is why proponents of steep emission cuts must abandon standard cost/benefit analysis, and instead recommend particular environmental targets (such as stabilizing atmospheric concentrations at a presumed “safe” level) and then try to find the least-cost method of attaining them.

As a final point, we should note how the problem of leakage also influences the “social cost of carbon” as computed in various models. When Nordhaus or other economists calculate the social cost of carbon (SCC), they are asking what happens to the present discounted value of future environmental damages, if someone emits an additional ton of carbon today, while holding the assumed trajectory of all future emissions constant.

Now we see the weakness in this metric, when trying to assess the net benefits of unilateral climate policy. Once we take leakage into account, we see that the standard measure of SCC overstates (possibly grossly so) the true costs to society from an additional unit of emissions. In reality, there are two things going on: When a U.S. manufacturer produces more units of a carbon-intensive good, it is true that he emits more carbon dioxide into the atmosphere. This is what the SCC looks at, and judges him accordingly.

However, the U.S. manufacturer also pushes down the world price of the good in question, and that tends to cause other producers to emit less CO2. Thus, there is a positive externality laid on top of the negative externality. The greater the scope for leakage, the greater the positive externality. In the extreme, where U.S. operations would be completely outsourced to China (in terms of carbon emissions, if not output of final goods), then the correctly measured “social cost of carbon” for U.S. operations would be zero, in the context of a unilateral U.S. cap.

Conclusion. Here are the takeaway messages:

(A) If the U.S. implements Waxman-Markey unilaterally, the environmental benefits will be even less than indicated by Chip Knappenberger’s pessimistic analysis.No matter how you slice it, Waxman-Markey fails standard cost/benefit tests. W-M advocates are certainly free to criticize standard cost/benefit tests, but they can’t stop there. They still need to justify quantitatively the steep emission targets in W-M. And to the extent that they invoke U.S. leadership in prodding the rest of the world to follow suit, proponents also need to come up with a plausible story showing the likelihood of worldwide action, with and without Waxman-Markey, versus some other possible U.S. approach.

(B) If the whole world implements Waxman-Markey, then the loss to economic output will far exceed the reduction in expected environmental damages.

Yet W-M proponents have done none of these things. Surely they could at least try–even in an informal blog post–to formalize their case, before expecting the American people to sign on to a plan that could cost trillions of dollars in forfeited economic growth, and which on its face will do very little to alter the course of global warming.

Subscribe to:

Posts (Atom)